Feb 17, 2026

Feb 17, 2026 0 Comment

0 Comment

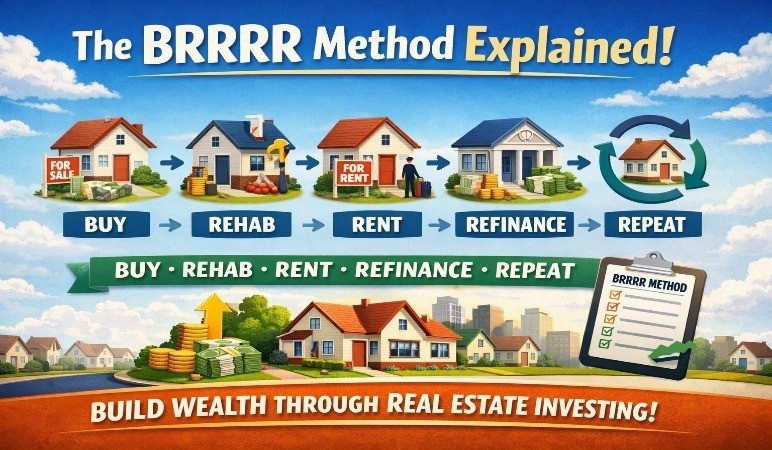

BRRRR Method Explained: Buy, Rehab, Rent, Refinance, Repeat

What Is the BRRRR Method?

The BRRRR method is a real estate investment strategy that allows you to build a rental portfolio with limited capital by recycling the same money through multiple properties. Instead of tying up cash in each property you buy, you pull most of it back out through refinancing and use it to buy the next one.

Here's the basic concept: Buy a distressed property below market value, fix it up, rent it out, refinance based on the new higher value, and use the cash-out proceeds to repeat the process. If executed properly, you can build a multi-property portfolio with the same initial capital.

The Five Steps of BRRRR Step 1: Buy

Purchase a property below market value. The key to BRRRR success starts here—you need to buy properties with significant upside potential.

What to Look For:

• Distressed properties needing cosmetic or moderate repairs

• Motivated sellers (foreclosures, divorces, probate)

• Properties priced 20-30% below after-repair value (ARV)

• Good neighborhoods with strong rental demand

• Properties where you can add value through improvements

Financing Options:

• Cash (fastest, most competitive)

• Hard money loans (12-15% interest, short-term)

• Private lenders

• Home equity lines of credit (HELOC)

• FHA 203(k) loans (for owner-occupants willing to live there during rehab)

Step 2: Rehab

Renovate the property to increase its value and make it rent-ready. Speed and budget control are critical here.

Focus on High-Impact Improvements:

• Kitchen updates (new cabinets, countertops, appliances)

• Bathroom renovations

• Fresh paint throughout (neutral colors)

• New flooring (vinyl plank, carpet)

• Updated fixtures and lighting

• Curb appeal (landscaping, front door, mailbox)

Avoid Over-Improving:

Don't add luxury finishes to a mid-range neighborhood. Your goal is to bring the property to market standard, not exceed it. Remember, you're creating a rental, not your dream home.

Timeline Goal: 30-60 days for most rehabs. Every month you hold costs you money in loan interest, utilities, and opportunity cost.

Step 3: Rent

Place a quality tenant and establish rental income. This step proves to lenders that the property generates cash flow.

Setting the Right Rent:

• Research comparable rentals in the area

• Price competitively to fill quickly

• Consider offering 1-2 months free rent for longer lease terms

Tenant Screening:

Don't rush this step. A bad tenant can destroy your BRRRR profits. Verify:

• Credit score (aim for 600+)

• Income (3x monthly rent minimum)

• Rental history (call previous landlords)

• Criminal background

• Employment verification

Lease Duration: Most lenders require at least 6-12 months of rental history before refinancing, though some accept a signed lease.

Step 4: Refinance

This is where the magic happens. You refinance from your high-interest acquisition loan into a conventional mortgage based on the property's new, higher value.

How Refinancing Works:

Most lenders will allow you to borrow 75% of the property's appraised value (called Loan-to-Value or LTV). If you bought well and renovated smartly, this new loan should cover most or all of your initial investment.

Example:

• Purchase price: $150,000

• Rehab costs: $30,000

• Total invested: $180,000

• After-repair value (ARV): $250,000

• Refinance at 75% LTV: $187,500

• Cash out: $187,500 - closing costs (~$5,000) = $182,500

• You pulled out $182,500 on a $180,000 investment

You now own a cash-flowing rental property with virtually no money left in the deal.

Refinance Requirements:

• Property must appraise at sufficient value

• Good credit score (typically 620+)

• Debt-to-income ratio below 43-50%

• 6-12 months of seasoning (ownership) depending on lender

• Property must cash flow

Step 5: Repeat

Take the cash you pulled out and do it again. And again. And again.

With $180,000 in capital, you could potentially acquire:

• Property 1: Years 1-2

• Property 2: Years 2-3 (using refinanced capital)

• Property 3: Years 3-4

• Property 4: Years 4-5

In 5 years, you could control 4+ rental properties, each producing cash flow and appreciating in value.

Real-World BRRRR Example

Property Purchase:

• Address: 3-bedroom single-family in growing suburb

• Purchase price: $140,000 (20% below market)

• Closing costs: $4,000

• Financing: Hard money loan at 12% interest

Rehab Phase:

• Kitchen: $12,000 (new cabinets, countertops, appliances)

• Bathrooms: $8,000 (2 full baths updated)

• Flooring: $6,000 (luxury vinyl throughout)

• Paint/fixtures: $4,000

• Landscaping: $2,000

• Total rehab: $32,000

• Timeline: 45 days

Rent Phase:

• Market rent research: $1,600-$1,800/month

• Listed at: $1,700/month

• Tenant placed: 10 days

• Lease term: 12 months

Refinance Phase:

• Waited 6 months for seasoning

• New appraisal: $235,000

• 75% LTV loan: $176,250

• Refinance costs: $4,500

• Cash pulled out: $176,250 - $144,000 (payoff hard money) - $4,500 = $27,750

Results:

• Total invested: $176,000 ($140K + $32K + $4K)

• Left in deal after refinance: $148,250

• Monthly cash flow: $350 (after mortgage, taxes, insurance, maintenance reserves)

• Annual return on remaining capital: 2.8% cash-on-cash

• PLUS: Appreciation, mortgage paydown, tax benefits

Common BRRRR Mistakes and How to Avoid Them 1. Buying at the Wrong Price

The biggest mistake: overpaying. BRRRR only works when you buy below market value. Use the 70% rule: pay no more than 70% of ARV minus rehab costs.

Formula: Maximum Purchase Price = (ARV × 0.70) - Rehab Costs

2. Underestimating Rehab Costs

Always add 20% buffer to your contractor's estimate. Hidden issues always emerge. Budget for:

• Permit fees

• Code violations

• Hidden damage

• Contractor delays

• Material cost increases

3. Slow Rehab Timeline

Every extra month costs you interest, utilities, insurance, and opportunity cost. Stay on top of contractors. Visit the property weekly. Have materials ready before work begins.

4. Poor Tenant Selection

A bad tenant can cost you $10,000+ in lost rent, eviction costs, and repairs. Never skip screening to fill vacancy faster.

5. Appraisal Coming in Low

If the property doesn't appraise high enough, you can't pull out your capital. Prevent this by:

• Using professional quality finishes

• Providing the appraiser with comparable sales

• Ensuring property matches neighborhood standards

• Taking high-quality photos for appraisal

6. Running Out of Cash

Keep reserves for unexpected costs. Don't invest your last dollar. Aim to keep 6 months of holding costs in reserve.

BRRRR vs. Traditional Buy-and-Hold

Traditional Buy-and-Hold:

• Buy turnkey property

• Put down 20-25%

• Capital stays locked in property

• Build portfolio slowly over many years

BRRRR Method:

• Buy distressed property

• Add value through rehab

• Pull capital back out

• Reuse same capital multiple times

• Build portfolio 2-3x faster

Is BRRRR Right for You?

BRRRR works best if you:

• Have limited capital but want to scale quickly

• Can find below-market deals

• Have rehab experience or good contractors

• Are willing to put in extra work upfront

• Want to maximize leverage and returns

BRRRR may not work if you:

• Can't find good deals in your market

• Don't have rehab skills or reliable contractors

• Need immediate cash flow

• Want passive, hands-off investing

• Have poor credit or high debt

Final Thoughts

The BRRRR method is powerful but not passive. It requires work, skill, and patience. However, for motivated investors willing to learn and execute, it's one of the fastest paths to building a substantial rental portfolio.

Start with one property. Master the process. Learn from mistakes. Then scale.

Remember: wealth is built property by property, refinance by refinance, year by year. The BRRRR method just accelerates the timeline.

0 Comment